Yes, you can finance one — and for a $5,000 Sur-Ron or a $9,000 Storm Bee, most buyers do. But financing a dirt bike is not like financing a car, and the "as low as $X/month" banner on a dealer page hides more than it shows. Here are the real options, the honest cost of the interest, and the one situation where financing genuinely makes sense — from the site that tells you when not to spend.

The short answer

Mid-tier and premium electric dirt bikes (roughly $3,000+) are widely financeable through dealers; budget and kids' bikes usually aren't (and shouldn't need to be). Your realistic options are buy-now-pay-later at checkout or a powersports installment loan. Both are convenient. Both cost real money unless you catch a true 0% promo and clear it on time. Finance a bike you'll actually use hard enough to justify — ideally a street-legal one that offsets driving costs — and avoid stretching for a toy you can't yet afford.

Your financing options, ranked by what they really cost

1. Buy-now-pay-later (Affirm, Klarna, Sezzle). The most common option on e-moto dealer checkouts. Fast approval, often a soft credit pull, and sometimes a genuine 0% promo on shorter terms. The catch: outside the promo, APRs range widely (roughly 0-36%), and some plans use deferred interest — miss the payoff and you owe all the back-interest at once. Best for buyers with good credit who will clear the balance inside the promotional window.

2. Powersports / dealer installment loan. A traditional fixed-term loan (24-60 months) through a powersports lender. Predictable monthly payment, but APRs typically run ~10-25%+ depending on credit, and off-road-only bikes can be harder to place than street-legal ones because there's no title to secure the loan. Best when you want a fixed payment and can't clear a BNPL promo in time.

3. Personal loan or credit union loan. An unsecured personal loan from your bank or credit union is often cheaper than powersports financing if your credit is decent, and it's title-agnostic (the lender doesn't care that it's an off-road bike). Worth a five-minute rate check before you accept dealer financing.

4. Credit card. Convenient and sometimes rewards-earning, but standard card APRs (often 20-29%) make this the most expensive way to carry a balance. Fine only if you'll pay it off that month — otherwise the worst option here.

The real cost of interest (the honest math)

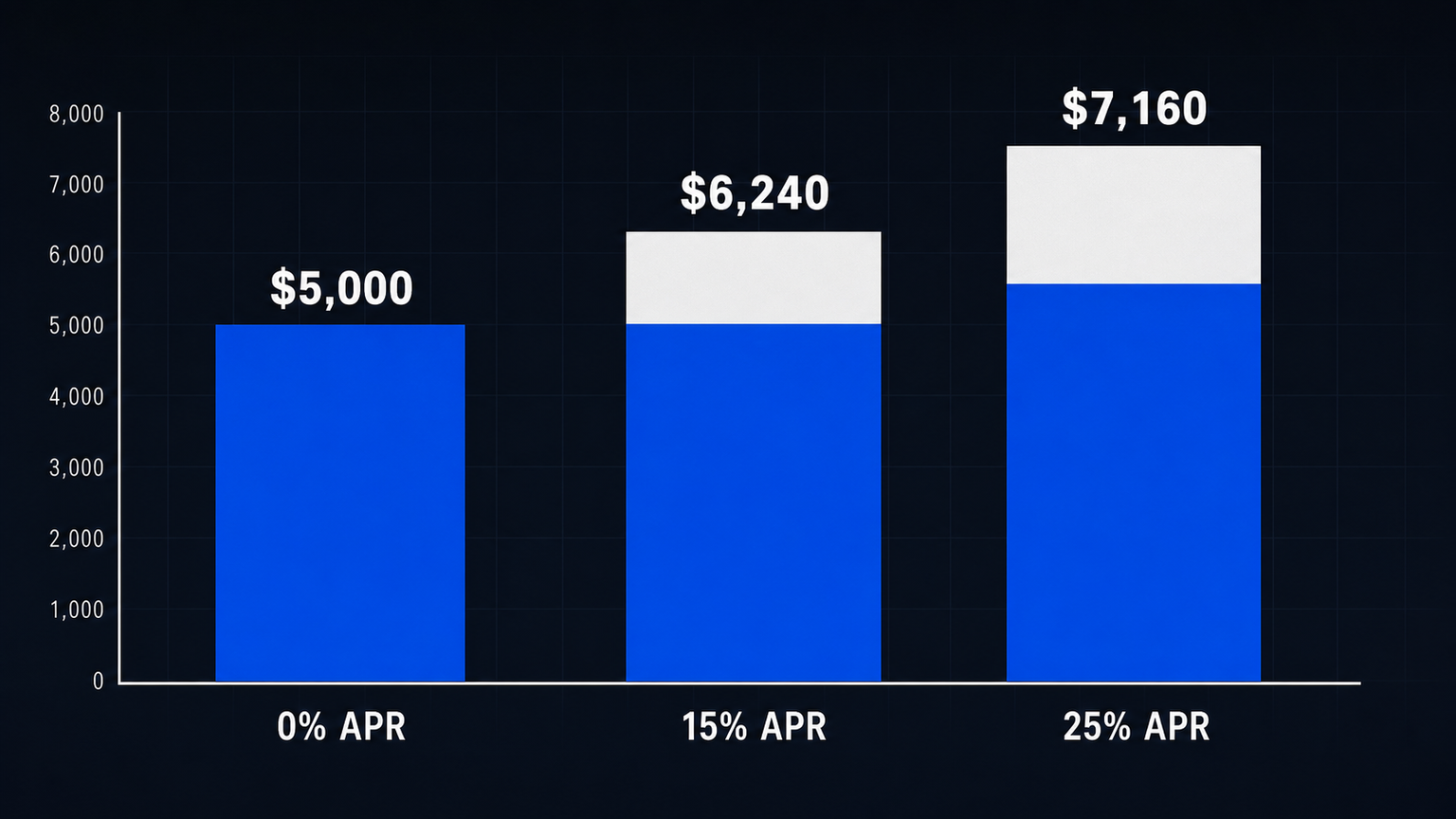

Dealers advertise the monthly payment, not the total. Here's what a $5,000 bike over 36 months actually costs:

| APR | Monthly payment | Total paid | Extra vs. cash |

|---|---|---|---|

| 0% (true promo) | ~$139 | ~$5,000 | $0 |

| 15% | ~$173 | ~$6,240 | ~$1,240 |

| 25% | ~$199 | ~$7,160 | ~$2,160 |

At 25% APR, you pay for almost half a second bike in interest. On a $9,000 Storm Bee the gap is nearly double that. This is the number the "$139/month!" banner is designed to keep you from calculating — so calculate it.

Should you finance? The honest answer

We're an independent site, so we'll say the part the dealers won't: financing a depreciating off-road toy is an expensive way to buy fun. A dirt bike loses value the moment it's ridden, it can't earn you anything, and if money is tight enough that you need 36 months to afford it, you probably can't yet afford the running costs (tires, brakes, a $1,600-3,000 battery someday) either. If you can save two or three months and pay cash, do that — you'll spend hundreds to over a thousand dollars less and own it free and clear.

The one real exception: a street-legal bike you'll genuinely commute on. If an Onyx RCR or a converted Sur-Ron replaces car trips, gas, and parking, the monthly payment can be offset by money you're no longer spending on a car — and then financing can pencil out. That's a transportation decision, not a toy purchase, and it's the case where a fixed monthly payment is defensible.

And if you do finance: chase a true 0% promo (not deferred interest), set autopay to clear it before the window closes, put down as much as you can to shrink the interest base, and check a credit-union personal-loan rate before signing whatever the dealer offers.

What you'll need

- Credit: BNPL is the most forgiving (soft pull, wide approval); installment loans generally want ~640+ for reasonable terms; 0% promos want strong credit.

- A down payment: optional for BNPL, but every dollar down cuts the interest you'll pay.

- Proof of income for larger installment loans.

- Realistic budget: factor the total cost of ownership — gear, insurance if you register it, and eventual battery replacement — not just the sticker.

The bottom line

You can absolutely finance an electric dirt bike, and for the premium tier it's normal. Just buy with the total number in view, not the monthly one: at real-world APRs, financing a $5,000 bike adds $1,000-2,000 to the price. Pay cash if you can; use a true 0% promo you'll clear on time if you can't; and reserve multi-year financing for a street-legal bike that's genuinely replacing a car. Not sure which bike fits your budget in the first place? Start with the Find Your Ride configurator and our cost guide.

VoltRipper is reader-supported and independent. We may earn a commission if you use a financing or purchase link, at no extra cost to you — it never affects our advice, and our honest position is to pay cash when you can. Financing terms, APRs, and promotions vary by lender, credit, and date; confirm the exact terms before you sign. This is general information, not financial advice.

FAQ

Can you finance an electric dirt bike?

Yes. Most authorized dealers offer financing on the mid-and-premium tier — buy-now-pay-later (Affirm, Klarna, Sezzle) at checkout, or a powersports installment loan. Budget and kids' bikes (usually under $1,000) are typically cash or a credit card, not financed. Off-road-only bikes can be harder to finance through traditional powersports lenders than street-legal models, because there's no title to secure the loan.

What credit score do you need to finance a Sur-Ron or Talaria?

BNPL providers (Affirm, Klarna) approve a wide range of scores and often do a soft pull, with better rates above ~670. Powersports installment loans generally want fair-to-good credit (~640+) for reasonable terms; below that, expect high APRs or a required down payment. Promotional 0% offers almost always require strong credit.

Is 0% financing on an electric dirt bike really free?

It can be — if you pay it off within the promotional window. But many 0% and 'deferred interest' BNPL plans charge back ALL the accrued interest if you miss the payoff date or a payment, which can be steep. Read whether it's true 0% APR or deferred interest, and set autopay to clear it before the promo ends.

Should you finance an electric dirt bike?

For an off-road toy, be honest: financing a depreciating recreational vehicle at 15-25% APR is one of the more expensive ways to buy fun. If you can save and pay cash, you'll spend hundreds to over a thousand dollars less. Financing makes the most sense for a street-legal bike you'll actually commute on — where it offsets car, gas, and parking costs — or via a genuine 0% promo you'll clear on time.